Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

Posted Monday, May 27, 2024

Table Of Contents

We also have Tax Patrol! This is another wonderful tax service for those who don’t need business advisory services or real estate investment support, but from time to time want some love from an experienced tax consultant and business advisor. Have a quick tax question? Need to know the depreciation rules as you buy that new car? Wondering what your April tax bill is going to be in August? Your spouse upgraded to a different job- how is that going to affect things? You received a big bonus- yay, but how will that impact your tax bill?

We also have Tax Patrol! This is another wonderful tax service for those who don’t need business advisory services or real estate investment support, but from time to time want some love from an experienced tax consultant and business advisor. Have a quick tax question? Need to know the depreciation rules as you buy that new car? Wondering what your April tax bill is going to be in August? Your spouse upgraded to a different job- how is that going to affect things? You received a big bonus- yay, but how will that impact your tax bill?

| Keystone | Copper | Breck | |

| Individual Tax Return Prep (Form 1040, joint filing) [more] | |||

| Business Entity Tax Return Prep (Form 1065, 1120, 1120S) [more] | |||

| Household Tax Projection [more] | |||

| Business Tax Projections, PTET Calcs, SALT Workaround [more] | |||

| Estimated Tax Payments Calcs | |||

| Tax Resolution, Audit Defense [more] | Advanced | Advanced | Advanced |

| Complimentary Quick Chats (CQC) [more] | Routine | Routine | Routine |

| Annual Fee* | $1,740 | $2,400 | $3,360 |

| Paid Monthly | $145 | $200 | $280 |

| (prorated based on onboarding date) | |||

On one hand we have our Business Advisory Service plans which are very comprehensive yet might contain some services that not everyone needs such as salary optimization, payroll processing, multiple tax planning events, among other things.

On the other hand we have transactional relationships where clients come in each spring for tax return preparation, and that’s all they need. No questions. No tax planning. Just a pile of tax documents and a few discussions later and bada bing bada boom they have a tax return and a nice summer.

Is there an in-between? Boom! We have Investor Tax Patrol which is a fancy add-on to our Keystone Tax Patrol platform above.

Is there an in-between? Boom! We have Investor Tax Patrol which is a fancy add-on to our Keystone Tax Patrol platform above.

Investor Tax Patrol is a wonderful tax service for those who don’t need all the advisory bells and whistles, but desire tax planning and, at times, scenario-based decision making assistance from an experienced real estate CPA and tax consultant. Have a quick tax question? Need to know the depreciation rules as you furnish that new short-term rental? Want to kick around Real Estate Professional designation? Wondering what your April tax bill is going to be in August?

Consider these typical fees for a tax-only engagement for rental property tax return preparation. We'll get into an example in a bit-

Investor Patrol is specifically designed to give you the freedom to call, text or email us without the worry of being nickeled and dimed like other outdated CPA firms. And! We also provide a tax planning event (usually around May, June and July) where we gather up your financial records like paystubs, rental activities, stock sales, etc. and we create a mock tax return projecting your annual income and eventual tax obligations. We are not big on surprises… bad news in August is palatable, yet bad news on April 15 is unacceptable. Let’s not forget that Investor Patrol also includes IRS audit defense for any tax return that we prepare. Please review our full Investor Patrol Services webpage for all kinds of fine print for your consideration. It’s really not that much.

Investor Patrol is specifically designed to give you the freedom to call, text or email us without the worry of being nickeled and dimed like other outdated CPA firms. And! We also provide a tax planning event (usually around May, June and July) where we gather up your financial records like paystubs, rental activities, stock sales, etc. and we create a mock tax return projecting your annual income and eventual tax obligations. We are not big on surprises… bad news in August is palatable, yet bad news on April 15 is unacceptable. Let’s not forget that Investor Patrol also includes IRS audit defense for any tax return that we prepare. Please review our full Investor Patrol Services webpage for all kinds of fine print for your consideration. It’s really not that much.

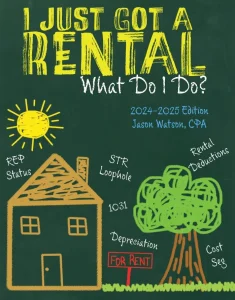

Also, please check out our rental property book titled I Just Got A Rental, What Do I Do? This is our second book. Our first book, Taxpayer’s Comprehensive Guide to LLCs and S Corps, was first published in 2014 and was well-received by small business owners and tax professionals, so we thought a book on rental properties and real estate investments would be equally helpful. So, here we are with our second iteration, or the 2025 edition. We plan to update annually.

With our Investor Patrol Services, everyone is a snowflake. Each real estate deal is unique, right? Each real estate investor is also unique. The above Investor Patrol Service plans are our attempt to give you an idea of the value proposition. Here are some pre-launch things we need to sort through-

Why do we have setup fees at all? We must ensure your prior depreciation is correct (especially if acquired with a 1031 exchange), all assets are correctly identified with original cost basis including acquisition costs, and loan amortization is properly recorded. We see a lot of junk out there which is not big deal until you want to sell the rental property, and minimize your tax pain.

Why do we charge extra for short-term rental setups? They are more intensive because there are more questions that need to be answered from us (and from you!), and we have to comb through furnishings and other boot up expenditures to ensure they are properly handled.

Why would I need a 3115 with a cost segregation study? If your rental property has already been in service and tax returns have been filed, then we need to request permission from the IRS to basically accelerate your depreciation on your current tax return. Alternatively we could amend your prior tax returns which is messy and expensive. Also, there is some tax arbitrage potentially if your income is higher today than it was when you first purchased your rental property. Lots to discuss here!

Why do we charge extra for a rental property acquired in a prior year 1031 like-kind exchange? We need to confirm that the previous tax professional computed the exchange correctly since once we prepare the tax return, we own the data including prior data.

You live in Colorado and have a rental property in California. You will need to file a California non-resident tax return even if the rental loses money. You have an income-generating asset in their state. Also, please consider that a taxing jurisdiction has the right to inspect your books and records to ensure your loss is truly a loss.

Keep in mind that some states and cities consider rental properties to be business ventures like any other, and more are focusing on short-term rentals as well. What makes things worse is that some taxing jurisdictions will impose an income tax based on gross rental receipts regardless if the activity is profitable. Yuck.

Here is some other complexity-

While we have your attention or perhaps even your interest, please read our State Problems With Your Rental Property section from our book “I Just Got A Rental, What Do I Do?”

These fees assume a 1040 tax return filing. At times, reporting your rental activities on a partnership tax return (Form 1065) might be a good idea to lower audit rate risk and mechanically show at-risk basis in the assets. Should a partnership exist such as a multi-member LLC owning rental properties that would be an add-on fee as shown above. (see our fee page for partnerships).

Here are some additional considerations during rental property tax return preparation.

Here are some additional considerations during rental property tax return preparation.

How does all this black magic work? With a cost segregation report, or some say a cost segregation study, all the sticks, bricks and stuff inside are figuratively torn down and put into different piles. Some piles (5-year or 7-year) are eligible for accelerated depreciation, another pile would be a 15-year pile which varies a bit, and the remaining pile will revert to the 27.5- or 39.0-year typical residential or nonresidential commercial use depreciation.

Technically, and with full-on geek-speak, cost segregation separates property elements that are “dedicated, decorative or removable” from those that are “necessary and ordinary for operation and maintenance of the building.” These piles are called asset classes, and they are maintained separately within your property’s depreciation schedule.

From there, and with the help of bonus depreciation and in some cases Section 179 expensing, you compress the multiple years of depreciation into one. Yay!

If your average guest stay is 7 days or less and you materially participate in the activity (500 hours, 100 hours and more than anyone else, or substantially all hours) you likely qualify for the short-term rental loophole. Given the intricacies with STRs, and additional time and diligence spent, we commonly have an add-on fee for these types of rental properties. We are short-term rental experts.

When you sell your rental property, including a 1031 or 721 exchange (don’t forget about Delaware Statutory Trusts), there will likely be an add-on fee of $250 for a straight-up sale or $500 to $750 for a like-kind exchange. This is where the rubber hits the road in terms of capital gains, and we need to spend the extra time to ensure a) your purchase price is correctly being considered including acquisition costs, b) improvements are accounted for and c) selling expenses and other things are factored in.

Our approach to starting off this relationship with you is to comprehensively understand your needs and objectives, and then design a malleable system as needed. Additionally, the following activities are considered out of scope and might incur a separate fee-

If we believe the requested service is outside of scope and not included in the Investor Patrol Services, we will have that awkward conversation with you ahead of time so an agreement can be reached. We will never do work and then bill you without an estimate of time from us and approval from you. In other words… ask away! It is up to us to pump the brakes with a “umm… yeah… can we chat about what’s involved for a bit first?”

The button below is a sample proposal for our real estate Investor Tax Patrol Service.

WCG CPAs & Advisors specializes in small businesses who generally have fewer than 25 employees. Why? We want to help people, and more importantly we want to help the business owner directly. Frankly speaking, once a business gets to a certain size management layers get in the way of owner access. Access allows us to ensure the owner(s) are leveraging the most out of their business for themselves and their families.

WCG CPAs & Advisors specializes in small businesses who generally have fewer than 25 employees. Why? We want to help people, and more importantly we want to help the business owner directly. Frankly speaking, once a business gets to a certain size management layers get in the way of owner access. Access allows us to ensure the owner(s) are leveraging the most out of their business for themselves and their families.

Because small business is a core competency for us, we have created Business Advisory Service platforms which include these really cool things-

Vail | Telluride | Aspen | |

Compliance & Preparation | |||

| Business Entity Tax Return (Form 1065, 1120, 1120S) [more] | |||

| Business Tax Projections (Franchise, Privilege, Receipts) | |||

| Individual Tax Return (Form 1040, joint filing) [more] | |||

| Tax Return Review Meeting | |||

| Tax Resolution, Audit Defense [more] | Advanced | Advanced | Advanced |

| State Income Apportionment, Nexus [more] | Add-On | Add-On | Add-On |

| Expat / Foreign Income Filings (FBAR, 8938) [more] | Add-On | Add-On | Add-On |

Strategic Tax Planning | |||

| Tax Advisory, Tax Reduction, Business Reviews [more] | 2 Sessions | 2 Sessions | Custom |

| Pre-Planning Meeting (May/Jun) | |||

| Household Tax Projections [more] | |||

| Business PTET Optimization [more] | |||

| Payroll Planning, Optimization [more] | |||

| Reasonable Shareholder Salary Calculation (RCReports) | |||

| Tax Projections Review Meeting (Jul/Aug) | |||

| Section 199A Deduction Optimization [more] | |||

| Small Business Tax Deductions Optimization [more] | |||

| Estimated Income Tax Calcs (via Payroll) [more] | |||

| End of Year Wrap-Up Meeting (Oct/Nov) [more] | |||

| Situational Tax Law Research (up to 3 hours) | |||

Payroll & Accounting | |||

| Monthly Shareholder Payroll Processing[more] | DIY | DIY | DIY |

| Quarterly QuickBooks Consulting (QuickStart) [more] | Add-On | Add-On | |

| Accounting Services (Bookkeeping + Analysis) [more] | Add-On | Add-On | Add-On |

| Financial Statement Review [Reach Reporting] | Inc with AST | Inc with AST | Inc with AST |

Business Advisory & Support | |||

| Periodic Quick Chats (May-Nov) [more] | 3 Chats | 3 Chats | Routine |

| Interfacing with Lenders, Attorneys, Planners | Add-On | Routine | Routine |

| CPA Concierge Services [more] | Add-On | Add-On | |

| Financial Analysis (Cash Flow, Budgeting, KPIs) | |||

| Annual Corporate Governance (Resolutions) | Add-On | Add-On | |

| Annual Fee* | $4,500 | $4,980 | Custom |

| Paid Monthly | $375 | $415 | Custom |

| (prorated based on onboarding date) | |||

We also have Tax Patrol! This is another wonderful tax service for those who don’t need business advisory services or real estate investment support, but from time to time want some love from an experienced tax consultant and business advisor. Have a quick tax question? Need to know the depreciation rules as you buy that new car? Wondering what your April tax bill is going to be in August? Your spouse upgraded to a different job- how is that going to affect things? You received a big bonus- yay, but how will that impact your tax bill?

| Keystone | Copper | Breck | |

| Individual Tax Return Prep (Form 1040, joint filing) [more] | |||

| Business Entity Tax Return Prep (Form 1065, 1120, 1120S) [more] | |||

| Household Tax Projection [more] | |||

| Business Tax Projections, PTET Calcs, SALT Workaround [more] | |||

| Estimated Tax Payments Calcs | |||

| Tax Resolution, Audit Defense [more] | Advanced | Advanced | Advanced |

| Complimentary Quick Chats (CQC) [more] | Routine | Routine | Routine |

| Annual Fee* | $1,740 | $2,400 | $3,360 |

| Paid Monthly | $145 | $200 | $280 |

| (prorated based on onboarding date) | |||

On one hand we have our Business Advisory Service plans which are very comprehensive yet might contain some services that not everyone needs such as salary optimization, payroll processing, multiple tax planning events, among other things.

On the other hand we have transactional relationships where clients come in each spring for tax return preparation, and that’s all they need. No questions. No tax planning. Just a pile of tax documents and a few discussions later and bada bing bada boom they have a tax return and a nice summer.

Is there an in-between? Boom! We have Investor Tax Patrol which is a fancy add-on to our Keystone Tax Patrol platform above.

Investor Tax Patrol is a wonderful tax service for those who don’t need all the advisory bells and whistles, but desire tax planning and, at times, scenario-based decision making assistance from an experienced real estate CPA and tax consultant. Have a quick tax question? Need to know the depreciation rules as you furnish that new short-term rental? Want to kick around Real Estate Professional designation? Wondering what your April tax bill is going to be in August?

Consider these typical fees for a tax-only engagement for rental property tax return preparation. We'll get into an example in a bit-

Investor Patrol is specifically designed to give you the freedom to call, text or email us without the worry of being nickeled and dimed like other outdated CPA firms. And! We also provide a tax planning event (usually around May, June and July) where we gather up your financial records like paystubs, rental activities, stock sales, etc. and we create a mock tax return projecting your annual income and eventual tax obligations. We are not big on surprises… bad news in August is palatable, yet bad news on April 15 is unacceptable. Let’s not forget that Investor Patrol also includes IRS audit defense for any tax return that we prepare. Please review our full Investor Patrol Services webpage for all kinds of fine print for your consideration. It’s really not that much.

Also, please check out our rental property book titled I Just Got A Rental, What Do I Do? This is our second book. Our first book, Taxpayer’s Comprehensive Guide to LLCs and S Corps, was first published in 2014 and was well-received by small business owners and tax professionals, so we thought a book on rental properties and real estate investments would be equally helpful. So, here we are with our second iteration, or the 2025 edition. We plan to update annually.

Here are some quickie FAQs to learn more about WCG CPAs & Advisors, and how we do business-

Nope. We have a t-shirt that reads, “Hate extensions. Love our summers.” We file 70% of our tax returns by April 15, and only extend per the client’s request or if there is missing data such as a rogue K-1. We’ll go as quickly as you let us! Also, we don’t have A listers… we prepare tax returns in first-in first-out sequence. Sure, we leave room for emergencies or other issues that allow for jumping the line.

Good question! Our Business Advisory Service plans (Vail, Telluride and Aspen) are more advisory forward like a robust old-fashioned with lots of planning, tax strategies and business consultation to help you make decisions. Our Tax Patrol Services (Keystone, Copper and Breck) are more tax return preparation forward like a refreshing vodka-lemonade with less tax planning, or at least less-intensive planning and consultation.

Investor Patrol Services for our rental property owners and investors is somewhere in-between since real estate is a business like any other requiring more tax planning, strategy and consultation but falls short of needing shareholder payroll planning and processing.

How Often Do We Schedule Meetings?

How Often Do We Schedule Meetings?Up to you, but within a structured framework! In the past, we tried rigid quarterly meetings, but they often felt like a chore for everyone. Then went full tilt the other way with a "call us anytime" approach. Duds on both sides.

Today, we operate on a 'Rhythm of the Relationship' model.

For Business Advisory clients, we generally connect about 8 times a year. This is a mix of strategic milestones where we reach out to you (Pre-Planning, Projections, Year-End Wrap-Ups) and On-Demand Support where you reach out to us (Tax Return Reviews, Advisory Sessions, and Scheduled Periodic Quick Chats). We provide the structure to keep you safe, but your goal is to use the on-demand access to extract everything you need.

And our Tax Patrol including Investor Patrol engagements can expect core strategic coverage including tax return reviews, pre-planning meeting, and tax projections, plus access to the same quick chats when life happens.

We prefer scheduled meetings over Teams. Check out our CPA Concierge Service as well. Priority boarding. HOV lane. Early check-in.

We rely heavily on emails and text message alerts. However, we do not have an allergy to the telephone. During friendly hours (let’s say 8AM to 7PM including weekends) we will usually call first if we have a question or need clarification.

Having said that, email can be an effective communication tool, and it is especially good for questions that require thought and good for memorializing conversations. While email is a chore for most people it can also be a distraction. Your WCG team is no different.

As such, we have two big rules that you need to be aware of-

When we have our amazingly productive and efficient conversation via Teams or phone call, we will always send a recap email to memorialize all the goodies. This recap email also gets captured by our workflow software allowing all other team members to view the recap as necessary.

For tax, we have two-person teams so there is always a backup. Teams are assigned based on who first spoke with you, bandwidth and subject matter expertise. We also have accounting, payroll and business formation / governance. As such, you might have 4 people you work with. Yay! The two tax peeps, and if applicable, a payroll peep to help with setup and training, and an accounting peep (if you are using our Accounting Services team for bookkeeping + analysis). We also have dedicated Client Support and Tax Support teams to… well… support you and the other teams.

Taxes can be tricky. Chat with a WCG human now and get questions answered.

Business Formation | |

| Articles of Organization or Incorporation, or Dissolution | $625 + state filing fee |

| Initial Report (if required) | $125 + state filing fee |

| Annual Report | $350 + state filing fee |

| Employer Identification Number (EIN) | Included |

| Single Member Operating Agreement (SMLLC) | Included |

| MS Word Templated Bylaws Agreement (Corporations) | Included |

| S Corp Election, Timely Election (made with formation) | Included |

| Accountable Plan | Included |

Onboarding Fees (one and done) | |

| Payroll Accounts Setup, Transfer, Closing | $550 to $650 depending on state |

| Payroll Quick Launch, Account Setup | $950 to $1,050 depending on state |

| Accounting Setup or Transfer (Fractional Controller) [more] | Varies |

| QuickStart, QuickBooks Setup and Support (90 days) [more] | $750 |

| S Corp Election, Timely Election (within 75 days) | $450 |

| Late S Corp Election Back to January 2024 [more] | $600, $1,200 after Jan 1 2024* |

| Examine Prior Tax Return | Included |

Business Maintenance | |

| Entity Relocation Package (payroll closure and opening, entity move) [more] | $1,850 (some are $2,100) + state filing fees |

| Address Changes w/o Payroll (IRS, State Dept of Revenue, Secretary of State) | $250 + state filing fees |

| Address Changes with Payroll (above + state and local payroll agencies) | $350 to $450 + state filing fees |

We are not salespeople. We are not putting lipstick on a pig, and trying to convince you to love it, even if Tom Ford’s Wild Ginger looks amazing. Our job remains being professionally detached, giving you information and letting you decide.

Moreover, many CPAs and tax professionals thrust their risk aversion onto their clients. This is bad. At WCG CPAs & Advisors we must perform our due diligence and hurdle our ethical and professional standards. However, after those gymnastics we present a risk-based analysis to the tax return and let you, the client and taxpayer, decide how to proceed. Having said that, we don’t entertain tax scammers or those who can take down the ship. Arthur Anderson anyone? No thanks.

Moreover, many CPAs and tax professionals thrust their risk aversion onto their clients. This is bad. At WCG CPAs & Advisors we must perform our due diligence and hurdle our ethical and professional standards. However, after those gymnastics we present a risk-based analysis to the tax return and let you, the client and taxpayer, decide how to proceed. Having said that, we don’t entertain tax scammers or those who can take down the ship. Arthur Anderson anyone? No thanks.

We also see far too many crazy schemes and half-baked ideas from attorneys and wealth managers. In some cases, they are good ideas. In most cases, all the entities, layering and mixed ownership is only the illusion of precision. Just because you can complicate the crap out of your life doesn’t mean you must. Just like Chris Rock says, just because you can drive your car with your feet doesn’t make it a good idea.

As mentioned elsewhere we primarily focus on small business owners and real estate investors, and their unique consultation and tax preparation needs. With over 90 full-time consultation professionals including Certified Public Accountants, Enrolled Agents and Certified Financial Planners on your team, WCG CPAs & Advisors consults on custom business structures, multiple entity arrangements, S corp elections (even late S corp elections back to January), tax strategies, business coaching, industry analysis, executive benefits, retirement planning including individual 401k plans, exit strategies, business valuations, income tax planning and modeling, and tax representation.

As mentioned elsewhere we primarily focus on small business owners and real estate investors, and their unique consultation and tax preparation needs. With over 90 full-time consultation professionals including Certified Public Accountants, Enrolled Agents and Certified Financial Planners on your team, WCG CPAs & Advisors consults on custom business structures, multiple entity arrangements, S corp elections (even late S corp elections back to January), tax strategies, business coaching, industry analysis, executive benefits, retirement planning including individual 401k plans, exit strategies, business valuations, income tax planning and modeling, and tax representation.

We also work with business law attorneys for business owners who have additional needs such as drafting Operating Agreements, fee for service contracts, buying or selling a business including employee stock ownership plans and partner buy-ins. In addition, WCG coordinates with third party plan administrators create age-based profit sharing plans and cash balance (defined benefit) plans. We can run point on whatever your business needs to ensure that communication is effective and efficient allowing you to sell widgets.

Here are some additional resources you might find useful.

Various Things | |

| Copying and returning of original tax documents | $45 |

| Significant changes or additions after a preliminary tax return is prepared- “crud, let me re-work all my numbers.” | $250 / hr |

| Tax resolution and/or audit assistance; Resolution is typically 2 hours; audit assistance is typically two 2-hour sessions | $375 / hr |

| Lender or “comfort” letters | $250 to $600 |

| Business Valuations | $5,000 – $8,000 retainer, $350 / hr |

| Divorce Analysis, Litigation Support | $250 / hr, $350 / hr for court |

| Client Support, Administrative billable rate | $150 / hr |

| Accountant billable rate | $150 / hr |

| Supervisor billable rate | $250 / hr |

| Manager billable rate | $300 / hr |

| Partner billable rate | $400 / hr |

| Managing Partner billable rate | $450 / hr |

| Senior Partner billable rate | $475 to $525 / hr |

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.