Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

Table Of Contents

Some businesses don’t fare as well as others when determining the exit plan. For example, you are a solo attorney working a lot of one and done cases such as divorce or DUIs where there is very little recurring revenue. This is difficult to sell or transition to others since most acquisitions involving personal services are based on future revenue. Take this same solo attorney and consider him or her an estate planning attorney who might have “maintenance agreements” with the clients; this dynamic of future recurring revenue now creates an economic benefit that another attorney might want to acquire. Boom! You’ve created an attraction that can be leveraged into succession.

Some businesses don’t fare as well as others when determining the exit plan. For example, you are a solo attorney working a lot of one and done cases such as divorce or DUIs where there is very little recurring revenue. This is difficult to sell or transition to others since most acquisitions involving personal services are based on future revenue. Take this same solo attorney and consider him or her an estate planning attorney who might have “maintenance agreements” with the clients; this dynamic of future recurring revenue now creates an economic benefit that another attorney might want to acquire. Boom! You’ve created an attraction that can be leveraged into succession.

WCG is currently exploring the poor man’s version of an ESOP where our primary entity is a C corporation which has a robust shareholder agreement for buying and selling of shares. While we are sacrificing the huge tax benefits of a true ESOP we are saving on costs and increasing our flexibility. One day we might convert to an ESOP just not today.

Why do you need a shareholder agreement? If you own 5% of a privately held small business you basically own 0%. Huh? Unless there is a market (public or private) where the minority shareholder can sell his or her shares, a 5% ownership in a privately held small business is not marketable and therefore not as valuable. In the business valuation world we call this degradation of value a discount for lack of control (DLOC) and a discount for lack of marketability (DLOM). Here is the IRS Job Aid on Discount for Lack of Marketability.

Why do you need a shareholder agreement? If you own 5% of a privately held small business you basically own 0%. Huh? Unless there is a market (public or private) where the minority shareholder can sell his or her shares, a 5% ownership in a privately held small business is not marketable and therefore not as valuable. In the business valuation world we call this degradation of value a discount for lack of control (DLOC) and a discount for lack of marketability (DLOM). Here is the IRS Job Aid on Discount for Lack of Marketability.

Therefore, a business needs to create a market both on the buy and sell side. For example, CPA firms typically are valued at about 1.0 to 1.5 times gross revenue depending on the quality of book of business (age of clientele, average fee, amount of recurring revenue, etc.). Using our example you could set up a program where an employee could buy shares using a valuation formula. Let’s say you have a CPA firm and you believe the factor is 1.2, and you also wanted to give your employees a 10% discount. You are growing and so you also want to use an average revenue number based on the previous two years to smooth out the value.

Your per share value formula would be (90% x Avg Revenue x 1.2) / number of authorized shares. This could be used for the buy side, and on the sell side.

On the buy side you could allow employees to purchase stock annually. You could also issue shares as a form of compensation (yes, that would find its way onto a W-2). You could also use this arrangement for a future owner where he or she pays some cash and obtains bank financing for the remainder allowing acquisition of a large chunk of stock. Many business-oriented banks will put together a deal where the new owner puts in 20% and the bank finances the 80% using the original owners as a backstop for collateralization. In other words, the sellers or original owners would promise to buy the stock back from the bank upon default, should it occur.

On the sell side you could allow employees to sell annually as well, and only upon separation from the business. By creating a market, a 5% minority ownership now has value. Some other considerations include that no person or entity other than current employees can own stock, and should an employee get divorced he or she cannot give the marital property to the other spouse.

Another consideration is voting rights. Do the minority shareholders have a vote? Perhaps by proxy? Ownership without a voice might not feel like ownership to your employees. How about wholesale sale? In other words, are the majority owners allowed to sell the entire business including the employees’ interests? Do the employees get a first right of refusal to buy out the majority owners?

Our example above was straightforward since CPA firms have enough market data to determine a gross revenue or sales factor. Other businesses use factors as well such as insurance agencies, financial advisor firms, franchised restaurants among several others. If a market approach to valuation using a gross revenue or sales factor cannot be used, a more complicated valuation approach or agreed-upon formula must be used. There are other factors too such as EBITDA (earnings before interest, tax, depreciation, amortization).

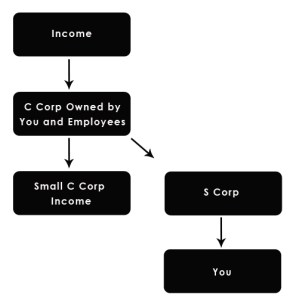

How does the current owner(s) pull money out? Our schematic to the right illustrates an arrangement that could be followed. We can get a bit nutty with the customization of this too… this is very simple but super flexible.

In our arrangement, income flows into the C corporation which is owned by you and your employees. A contractual arrangement would exist where the C Corp would pay your S Corp a management fee leaving a small amount of C corporation income behind (near zero).

This is a generalization and proper consultation with a tax professional (us) and an attorney (others) is a must.

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us