Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

Posted Friday, October 18, 2024

Table Of Contents

You show up to work on Friday and there’s a retirement cake in the breakroom. Interestingly, you are coming back on Monday as a 1099 contractor using the same computer at the same desk with the same lousy chair that tilts ever so slightly to the left. Let’s not forget the cracked and yellowing chair mat.

You show up to work on Friday and there’s a retirement cake in the breakroom. Interestingly, you are coming back on Monday as a 1099 contractor using the same computer at the same desk with the same lousy chair that tilts ever so slightly to the left. Let’s not forget the cracked and yellowing chair mat.

Why did this happen? Why did you get converted from a W-2 employee to an independent contractor suddenly needing a 1099 accountant? Many businesses like the flexibility of a gaggle of 1099 contractors. They can fill temporary voids in the workflow without a lot of commitment. They can save a bunch of money by not offering benefits such as health insurance, 401k match, unemployment and paid time off. They can lower their overall risk profile since independent contractors paid via a Form 1099-NEC are not protected like W-2 employees. Who is more fireable, right? A DOD contractor lays off 10,000 people and there are congressional hearings. 10,000 sub-contractors don’t get renewed and no one seems to care.

Is being an independent contractor a good thing? Yes! For two big reasons-

So, if your employer wants to be your client, and pay you as a contractor via on Form 1099-NEC, you might seriously consider it. Now what? You’ll need a 1099 accountant to help you budget your contractor income. Why?

A common complaint from independent contractors and those who own their own business is self-employment tax. Can you avoid, reduce, eliminate or lower your self-employment taxes or SE taxes? Ok, we just said two things that mean the same thing twice. Yes, you may reduce self-employment taxes to a large extent, but it takes some effort starting with an S Corp election (let’s not get ahead of ourselves yet).

If you are paid as a 1099 contractor, your income will be reported on your personal tax return (Form 1040) under Schedule C and is subject to self-employment tax (currently 15.3%) and ordinary income tax. So, by applying a 1099 tax calculator to your world, you could easily pay an average of 40% (15.3% in SE taxes + 24% in income taxes) on all your net contractor profits in federal taxes. Wow, that sucks!

If you are paid as a 1099 contractor, your income will be reported on your personal tax return (Form 1040) under Schedule C and is subject to self-employment tax (currently 15.3%) and ordinary income tax. So, by applying a 1099 tax calculator to your world, you could easily pay an average of 40% (15.3% in SE taxes + 24% in income taxes) on all your net contractor profits in federal taxes. Wow, that sucks!

Does creating a limited liability company (LLC) help avoid self-employment taxes? No, not automatically. A single member LLC is considered disregarded for tax purposes and your independent contractor activities will be reported on Schedule C. We are all humans, and we generally spend what we make. If you are not prepared for 30% to 40% in taxes for your 1099 contractor income, it could be a shocker on April 15. WCG CPAs & Advisors can help with tax reduction strategies and tax planning.

The “double” taxation should not be a stranger to you. When you were paid a W-2 salary of wage, you had Social Security and Medicare taxes taken out of your paycheck, and you also had income taxes withheld based on some payroll table. Income taxes were “negotiated” by tax deductions and credits (what used to be called exemptions vis a vis Form W-4). Social Security and Medicare taxes were imposed on your gross wages regardless.

What can be done to reduce self-employment taxes (aka, Social Security and Medicare taxes)? Enter the S Corp election on your 1099 independent contractor income. A 1099 S Corp if you will. Sounds fun, right?

Sidebar: The search term 1099 S Corp in 2008 had about 400 searches per month whereas in 2024 it is nearly 1,200 with over 5,400 in February. Independent contractor relationships are increasing dramatically.

Let’s dispel a common myth right away. An S corporation does not exist as an entity. You will not see it listed by any Secretary of State. It is a tax election. You need an underlying entity such as a limited liability company (LLC) or corporation (C Corp). When your LLC or corporation is taxed as an S Corp you are considered both an employee and a shareholder (think investor). As an employee being paid a salary, your income is subject to all the usual taxes that you would see on a paystub- federal taxes, state taxes, Social Security taxes, Medicare taxes, unemployment and state disability premiums.

However, as a shareholder or investor, you are simply getting a return on your investment. That income, or basically the remaining contractor profits after salary and expenses, is a form of investment income and therefore is not subject to self-employment taxes.

However, as a shareholder or investor, you are simply getting a return on your investment. That income, or basically the remaining contractor profits after salary and expenses, is a form of investment income and therefore is not subject to self-employment taxes.

As you recall, when we say self-employment taxes, we are really talking about Social Security and Medicare taxes. From a 1099 contractor perspective, they are self-employment taxes. From an employee perspective, they are Social Security and Medicare taxes. Same thing.

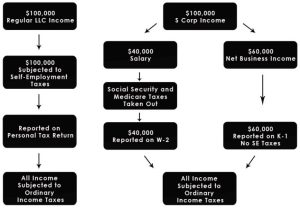

Let’s look at another visual in terms of how the 1099 money travels. The four boxes on the left are the money trail of your common contractor being paid via a Form 1099-NEC. The series of boxes on the right is the money trail of your entity being taxed as an S corporation, or as some might say, the 1099 S Corp. Note the $60,000 chunk of income on the far-right hand side that is not being taxed at the self-employment tax level. This is the source of your savings. Yay!

What is your net-net savings on all this gibberish? On $100,000 in 1099 contractor profits, you could save $8,000 to $10,000 in cash. On $250,000, you could save $15,000 to $18,000. The relationship is not purely linear, and it depends on your shareholder salary and how health insurance including health-savings accounts are being leveraged. We have a complete analysis of the tax savings of a 1099 S Corp in other webpages and from our book.

Also note that all your $100,000 is being subject to income taxes. This is a common misconception- a lot of contractors and business owners believe there is a magical income tax reduction with an S Corp election. Not true. The only reduction is in self-employment taxes. All other tax deductions such as operating expenses, home office expense, mileage, meals, self-employed health insurance, 401k plans, etc. are equally deductible with or without an S corporation election.

There are a handful of downsides to S Corps as well. Certain states are not attractive, additional accounting fees for tax preparation and payroll processing, among other things. Please review the 185 reasons S Corps stink from our book.

Naturally, you would want to pay a tiny salary to reduce the amount of income subject to Social Security and Medicare taxes, right? However, the IRS through Fact Sheet 2008-25 and a zillion tax court cases has enforced a reasonable shareholder salary standard. What does this mean? We have a webpage and an entire chapter from our book dedicated to this very question- what salary to pay yourself as a self-employed independent contractor.

Let’s say you are giving all this some thought, but would like to know how much to set aside for the looming tax bill. Without regards to your 1099 tax deductions and without knowing your overall household income, WCG CPAs & Advisors recommends setting aside about 20% to 25% of your gross 1099 earnings. Having said this, we are shooting in the dark and proper tax planning is a must.

Ahh.. the good stuff. Yes, you work hard. Yes, you want to be able to get a little extra from your hard work and your business. Yes, you want this to be tax-advantaged. We get it. Common self-employment tax deductions for most 1099 independent contractors include-

Ahh.. the good stuff. Yes, you work hard. Yes, you want to be able to get a little extra from your hard work and your business. Yes, you want this to be tax-advantaged. We get it. Common self-employment tax deductions for most 1099 independent contractors include-

However, there lots of other considerations such as 401k plans, health insurance, advertising, client gifts, country club dues, legal and professional fees, among other things. Keep in mind that self-employment tax deductions must be-

We want to give you this table to help summarize the business deductions that are clearly not allowed (black), the ones that clearly are allowed (white), and the gaggle of exceptions (grey). Please visit our chapter on small business tax deductions from our book.

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

![[page_title]](https://wcginc.com/wp-content/uploads/Reasonable-Salary.jpg)

![[page_title]](https://wcginc.com/wp-content/uploads/S-Corp-Life-Cycle-300x300-1.jpg)