Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

Table Of Contents

By Jason Watson, CPA

By Jason Watson, CPA

Posted Saturday, March 21, 2026

It is common to have a second home that you rent out. It is also common to have a rental property that you use personally. It’s all a matter of perspective, right? One of the biggest reasons to have a mixed-use rental property, or what the IRS would call personal use of a dwelling unit or vacation home, is to defray costs of ownership. Said in another way, a vacation home can be a nice split between current-day lifestyle enhancements and long-term wealth-building.

According to IRS Publication 527 Residential Rental Property–

You use a dwelling unit as a home during the tax year if you use it for personal purposes more than the greater of:

14 days, or

10% of the total days it is rented to others at a fair rental price.

If you trip these wires, the IRS considers the rental property (dwelling unit) a home. Why do you care about triggering these rules? If your rental property is partially considered to also be a residence (vacation home) then your expenses and therefore rental property deductions are limited. We’ll dig into what this means including the Bolton Tax Court case in a little bit

Let’s review the calculations first. You rent the property to others at a fair rental price for 67 days. The calculation above then becomes the greater of 14 days or 6.7 days. As such, you can use the property for 14 days as personal use and not trip the vacation home rules.

Another way to look at this- if you had 30 personal use days of your vacation home, then you would need to have rented it to others for 301 days or more. Why? You trigger the vacation home rules at the greater of 14 days or 10% of 301, or 30.1 days.

Let’s take a step back. There are two immediate questions. What is a day of personal use? What is fair rental price?

This is typically not a tough question to answer. AirDNA, Airbnb and VRBO can quickly help determine the fair rental price for short-term stays. Zillow, Realtor.com and others can also quickly help with long-term leases. There are a zillion other tools that we are not mentioning. Here is the blurb from IRS Publication 527 Residential Rental Property–

A fair rental price for your property is generally the amount of rent that a person who isn’t related to you would be willing to pay. The rent you charge isn’t a fair rental price if it is substantially less than the rents charged for other properties that are similar to your property in your area.

Ask yourself the following questions when comparing another property with yours.

Is it used for the same purpose?

Is it approximately the same size?

Is it in approximately the same condition?

Does it have similar furnishings?

Is it in a similar location?

If any of the answers are no, the properties probably aren’t similar.

We have a deep dive section on personal use days with your STR. However, here is a quick summary of the talking points-

Again, see our personal use of your short-term rental section for more information.

Let’s say you’ve determined that your personal use days exceed what is allowed and now vacation home rules apply. What are these silly rules anyway? IRC Section 280A(c)(5) reads in part-

(5) Limitation on deductions

In the case of a use described in paragraph (1), (2), or (4), and in the case of a use described in paragraph (3) where the dwelling unit is used by the taxpayer during the taxable year as a residence, the deductions allowed under this chapter for the taxable year by reason of being attributed to such use shall not exceed the excess of-

(A) the gross income derived from such use for the taxable year,

The first thing to do is calculate the rental use portion of the total days the property was used. Here is a table from a live WCG CPAs & Advisors client-

| Personal Use Days | 51 |

| Rental Use Days | 105 |

| Total Days of Property Use | 156 |

| Rental Use Portion | 67.3% |

| Personal Use Portion | 32.7% |

In this example, we will apply 67.3% to certain rental property expenses. However, there are several expenses that this rental use percentage will not be applied to-

Keep in mind that you must count actual rental use days as opposed to taking 365 days and simply deducting your personal use days.

Under vacation home rules, the personal use portion of mortgage interest and real estate property taxes are deductible on Schedule A of your Form 1040 (individual tax return). However, if your rental property tax deductions are going to be limited, you want the highest personal use portion to be applied to mortgage interest and property taxes.

What do we mean here? Look at the table above again. In that example, the rental property was rented for 105 days which would suggest there are “260 days-worth” of mortgage interest and real estate property taxes attributable to personal use, or about 71.2%, and not 32.7%.

The IRS would rather have you use the lower percentage since a higher amount of mortgage interest and property taxes would be applied to the rental and therefore limited under the vacation home rules (and in turn, not deductible). Consider this table-

| Mortgage Interest | 20,238 |

| Personal Use Portion (IRS Method) | 32.7% |

| Amount Deducted on Schedule A | 6,616 |

| Personal Use Portion (Tax Court Method) | 71.2% |

| Amount Deducted on Schedule A | 14,416 |

| Difference | 7,800 |

| Tax Rate | 37% |

| Cash Savings | 2,886 |

This is a big deal, right? It was for Dorance and Helen Bolton who owned a rental property in Palm Springs, California. In Bolton v. Commissioner, 77 Tax Court 104 (1981), the Tax Court stated-

Interest is an expense that accrues ratably over the year and property taxes may likewise be regarded as being applicable to the entire year. The ordinary and normal method of determining what portion of interest is allocable to any part of a year would be to multiply the annual interest by a fraction, the numerator of which is the number of days in the period involved and the denominator is the number of days in the year. The same process would be employed in respect of real estate taxes. It was this method that petitioner used in applying the limiting provisions of section 280A(c)(5)(B).

It continued to state-

In taking a different view, the Government utilizes the identical computation specified in section 280A(e)(1), in which it compresses the annual interest and property taxes into the 121-day period that the property was used. But while that computation may serve a useful purpose in respect of the otherwise nondeductible maintenance expenses that are ordinarily associated with occupancy or use of the property, entirely different considerations are involved in respect of items such as interest and taxes that are spread over the entire year and are deductible in any event.

What does all this mean? The Tax Court sided with Bolton who had basically computed a daily amount of mortgage interest and real estate property taxes, and deducted the amount associated with rental days from their rental income, and then deducted the remainder on Schedule A.

Sidebar: The Commissioner (IRS) appealed, and the United States Court of Appeals for the Ninth Circuit in 1982 affirmed the Tax Court’s decision.

As such, we now have a thing called the Tax Court Method and it is sometimes called the Bolton Method. A win for the taxpayer! The IRS really hated this loss. A lot.

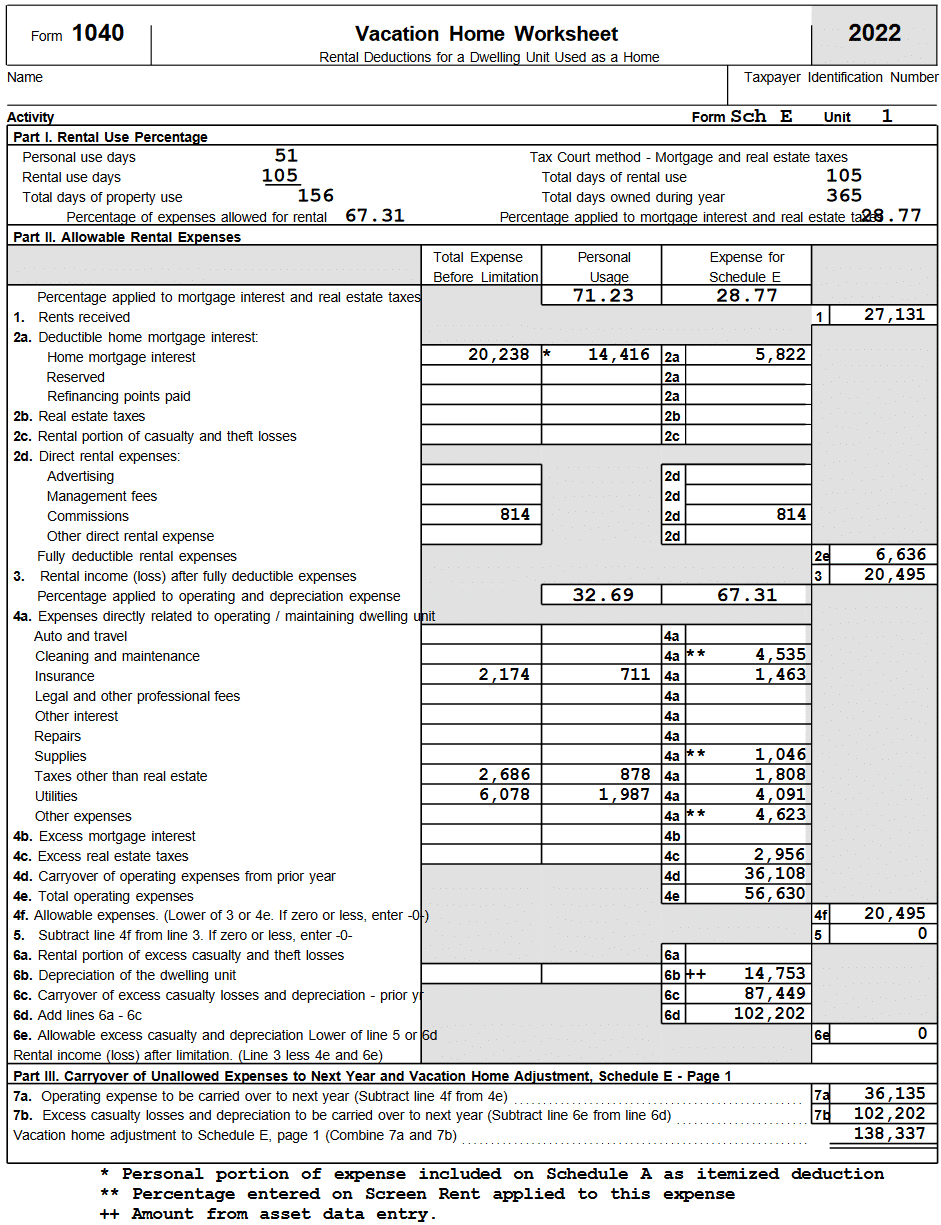

There is an iterative process to determining the eligibility to deduct certain rental property expenses. Worksheet 5-1. Worksheet for Figuring Rental Deductions for a Dwelling Unit Used as a Home from IRS Publication 527 Residential Rental Property walks you through the process. We will try to simplify it here-

As such you can see, you could possibly be calculating two carryover amounts for future years: operating expenses and depreciation.

Here is the worksheet from our tax software for a WCG CPAs & Advisors real estate investor-

A few notables on this Vacation Home Worksheet-

A few notables on this Vacation Home Worksheet-

You can see a PDF of this worksheet.

Keep in mind that these carryover amounts are not passive activity losses which are traditionally reported on Form 8582. Also, they cannot be used like passive activity loss carryovers upon sale. However, vacation home carryovers may be used when there is future rental income (profits).

Jason Watson, CPA, is a partner and the CEO of WCG CPAs & Advisors, a boutique yet progressive tax, accounting and rental property consultation and real estate CPA firm with over 90 team members and 7 partners headquartered in Colorado serving real estate investors worldwide.

This KB article is an excerpt from our 530+ page book (yeah, thick, there are some picture pages, but no scratch and sniff) which was updated April 5, 2026, and is available in paperback from Amazon, as an eBook for Kindle and as a PDF from ClickBank. We used to publish with iTunes and Nook, but keeping up with two different formats was brutal. You can cruise through these KB articles online, click on the fancy buttons below or visit our webpage which provides more information.

This KB article is an excerpt from our 530+ page book (yeah, thick, there are some picture pages, but no scratch and sniff) which was updated April 5, 2026, and is available in paperback from Amazon, as an eBook for Kindle and as a PDF from ClickBank. We used to publish with iTunes and Nook, but keeping up with two different formats was brutal. You can cruise through these KB articles online, click on the fancy buttons below or visit our webpage which provides more information.

|  |  |

| $32.95 | $21.95 | $18.95 |

Taxes can be tricky. Chat with a WCG human now and get questions answered.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.