Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

Posted Saturday, November 1, 2025

Table Of Contents

The holidays are coming and people start thinking about year-end moves to minimize their taxes. Every day between Christmas and New Year’s Day we field a zillion questions on year-end tax planning. While some ideas are great, there are pitfalls and sucker-holes. We’ll talk about tax deductions in general. We’ll talk about last-minute tax moves. And Yes, we’ll talk about automobiles. They always seem to top the list of good ideas (or at least most business owners think so).

The holidays are coming and people start thinking about year-end moves to minimize their taxes. Every day between Christmas and New Year’s Day we field a zillion questions on year-end tax planning. While some ideas are great, there are pitfalls and sucker-holes. We’ll talk about tax deductions in general. We’ll talk about last-minute tax moves. And Yes, we’ll talk about automobiles. They always seem to top the list of good ideas (or at least most business owners think so).

Also, we have separate Tax Reduction and Advanced Tax Strategies articles that is more aimed at general tax reduction strategies and not necessarily year-end tax moves. However, there is a lot of overlap.

There are two big objectives with end-of-year tax planning-

Please don’t forget the “make plans for 2026” part since big changes in business income or other events in your life need to be addressed early, and perhaps before April 15, 2026 for Q1’s estimated tax payment. As such we will talk about this first.

If your business income is going to be higher in 2026 than 2025, then we should get a jump on your business tax planning with these considerations. Remember, there is no such thing as an accounting emergency; only poor planning.

California is an easy target, but there are several other states which impose a franchise tax or some sort of “pleasure to do business in our state” tax. Additionally, these taxes are similar to income taxes where they must be paid quarterly in advance otherwise underpayment penalties and interest might be incurred.

PTET in a nutshell is the ability to pay your “human” state income taxes with business funds and thereby create a tax deduction for the business and eventually you as the owner. We discuss this in greater detail later. For now, there are two possible PTET dangers here so please pay attention- first, if 2026 is the first year of your pass-through entity such as an S corporation or partnership, and you want to participate in your state’s PTET program, then business tax planning is a must. Payments must be made on time (April, June, September, December) and in some cases, a timely registration and election must be made. For example, if you don’t register or “elect in” for New York by March 15, then you are out of luck for all of 2026 (there is some legislation that might extend this for New Yorkers to September 15).

PTET in a nutshell is the ability to pay your “human” state income taxes with business funds and thereby create a tax deduction for the business and eventually you as the owner. We discuss this in greater detail later. For now, there are two possible PTET dangers here so please pay attention- first, if 2026 is the first year of your pass-through entity such as an S corporation or partnership, and you want to participate in your state’s PTET program, then business tax planning is a must. Payments must be made on time (April, June, September, December) and in some cases, a timely registration and election must be made. For example, if you don’t register or “elect in” for New York by March 15, then you are out of luck for all of 2026 (there is some legislation that might extend this for New Yorkers to September 15).

Second, if 2026 is going to be more profitable than 2025, then your PTET payments need to be increased to prevent underpayment penalties and interest. For example, you converted from W-2 to 1099 contractor in the summer of 2025, and 2026 is going to be the first full-year with your new contractor status, a business tax plan needs to be updated to account for your increased 2026 PTET payments (and likely your franchise tax or business tax imposed by the state).

With the passage of the One Big Beautiful Bill Act on July 4, 2025, the state and local tax limit is now $40,000 for those households with $500,000 or less in income. Above that, it phases down to $10,000. We mention this because the PTET deduction remains valuable for many business owners with S Corps and partnerships.

If your business profit will jump up in 2026 as compared to 2025, then we must adjust your reasonable salary to accommodate for this change. More importantly, we must adjust your federal and state income tax withholdings. If we wait until tax planning season (May, June, July), two bad things happen- first, you get used to this new cash flow and start spending it, and second, the compression of waiting too long makes catching up painful.

Sooner than later is the motto.

January is a great time to update your 2026 business tax plan, but only if there is a material difference between 2025 and 2026. If you call up and say, “hey, my business is going to be up 5%, can I get an updated business tax plan?” We will say “Yes, absolutely… but let’s wait until summer.” January business tax planning is very compressed, and therefore we kindly want to reserve it for those who truly need it.

Otherwise, if you are curious about your Q1 or Q2 franchise or business tax, or your PTET payment, please use 2025 as a proxy for 2026 until we can tweak with an updated business tax plan in the summer.

Here is a comparison table for your perusal-

| | 2025 | 2026 |

| IRA | 7,000 | 7,500 |

| Roth IRA Income Limits | 150,000 single | Update in Dec |

| | 236,000 married | Update in Dec |

| 401k Employee | 23,500 | 24,500 |

| HSA Contribution | 4,300 self | 4,400 self |

| | 8,550 family | 8,750 family |

| Social Security Wage Limit | 176,100 | 184,500 |

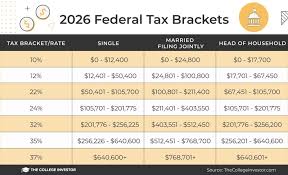

| Standard Deduction | 15,750 single | 16,100 single |

| | 31,500 married | 32,200 married |

| Gift Limit | 19,000 | 19,000 |

| Foreign Income Exclusion | 130,000 | 132,900 |

| Mileage Deduction | 70 cents | Update in Dec |

Quick lesson on tax deductions. When you write a check and it has a tax savings element (401k, IRA, charity, etc.) it is not a dollar-for-dollar savings. For example, if you are in the 22% marginal tax bracket, you must write a check for $4,000 just to save $880 in taxes. Keep this in mind as you read this information on year-end tax savings. Also keep in mind that cash is king, and that perhaps paying a few more taxes today with the added flexibility of cash in the bank can be comforting.

Quick lesson on tax deductions. When you write a check and it has a tax savings element (401k, IRA, charity, etc.) it is not a dollar-for-dollar savings. For example, if you are in the 22% marginal tax bracket, you must write a check for $4,000 just to save $880 in taxes. Keep this in mind as you read this information on year-end tax savings. Also keep in mind that cash is king, and that perhaps paying a few more taxes today with the added flexibility of cash in the bank can be comforting.

Another way to look at it is this- most people say “I want to save taxes” but really what they are saying is “I want to save cash.” In other words, most people are in the cash-saving business not the tax-saving business. If we can do both, great. However, most tax-savings moves take cash, and cash is what you want to keep. So, keep this concept in mind as review some of the year-end tax moves listed below.

Also!

Tax deductions and tax deferrals are not the same. Tax deferrals are tax bombs later in life; little IOU’s to the IRS and they will eventually call in the chit. But if you use the immediate tax savings to build wealth, then a tax deferral is worth it. Deferring taxes to pay for a cruise vacation might not always be the best approach (then again, live a little!).

Wait, there’s more!

Just because you go $1 into the next tax bracket does not mean all your dollars are taxed at that rate. So, if you are trying to thread the needle with a Roth conversion to not fly too close to the sun out of fear of blowing up your tax world, don’t sweat it too much. Sure, if you push $25,000 into the 32% marginal tax bracket when you could have delayed until next year, that is an 8% x $25,000 or a $2,000 mistake. Sidebar- the 8% is 32% less 24%.

The deduction for what you pay in state and local income, sales and property taxes is also getting squeezed. This is commonly referred to as SALT deductions (State And Local Tax). People commonly say SALT deductions and property taxes. Property taxes are inclusive of state and local tax… it is like saying drugs and alcohol. Alcohol is a drug. SALT deductions include all taxes imposed by your state or local jurisdiction. This was defined as such by the Revenue Act of 1913 and later clarified in 1964. Riveting. But somehow we’ve managed to say SALT deductions and property taxes as separate items. At least it is not as bad as saying ATM Machine or ABS Brakes. Who says that? We digress…

The Tax Cuts and Jobs Act of 2017, back when Despacito was the big hit, limited the amount of SALT deductions on Schedule A of your Form 1040 (individual tax return) to $10,000. With the passage of the One Big Beautiful Bill, SALT is now up to $40,000 for those married tax filers with $500,000 or less in adjusted gross income (AGI). Therefore, if you have property taxes of $15,000 and California income tax of $30,000, you are only able to deduct $40,000 of this $45,000. This leaves $5,000 on the table, or about $1,200 if you are in the 24% marginal tax bracket.

The Tax Cuts and Jobs Act of 2017, back when Despacito was the big hit, limited the amount of SALT deductions on Schedule A of your Form 1040 (individual tax return) to $10,000. With the passage of the One Big Beautiful Bill, SALT is now up to $40,000 for those married tax filers with $500,000 or less in adjusted gross income (AGI). Therefore, if you have property taxes of $15,000 and California income tax of $30,000, you are only able to deduct $40,000 of this $45,000. This leaves $5,000 on the table, or about $1,200 if you are in the 24% marginal tax bracket.

This example is not uncommon since for you to have $30,000 in California income tax, the household would have about $400,000 in taxable income. But if your household income is suddenly $600,000, then your SALT limit is $10,000 (yeah, quite the cliff) and your California tax might be $49,000ish. So, suddenly PTET and great SALT work around are back in business.

As alluded to, there is a work-around for business owners of S Corporations and Partnerships, or what we call pass-through entities or PTEs. About 37 states are allowing business owners to make a tax payment to the state based on net business income. This does two things-

The IRS took note of the workaround, but understood it was perfectly legit. The IRS through Notice 2020-75 states,

Certain jurisdictions described in section 164(b)(2) have enacted, or are contemplating the enactment of, tax laws that impose either a mandatory or elective entity-level income tax on partnerships and S corporations that do business in the jurisdiction or have income derived from or connected with sources within the jurisdiction. In certain instances, the jurisdiction’s tax law provides a corresponding or offsetting, owner-level tax benefit, such as a full or partial credit, deduction, or exclusion.

The IRS continues by stating this practice is permitted under the notice until it can legislate this practice into regulations. Also, there are all kinds of rules, and not every business owner will benefit from making a pass-through entity tax election. As such, the tax planning for determining the efficacy of using this tax deduction is challenging.

Wow. That was a lot of gibberish, huh? Talk to your favorite tax pro at WCG CPAs & Advisors, and make sure you understand this amazing workaround for tax deductions being truncated by SALT limits. The cocktail party fodder term is “PTET election” or “SALT workaround,” where PTET stands for pass-through entity tax. There are some devils in the details, and not all states work the same. Yes, we are as surprised as you are.

Some taxpayers have their refunds kept by the IRS because of back taxes, or other obligations such as student loans. In these situations, you can put yourself in a “tax due” position by decreasing your withholdings on your pay checks and putting more money in your pocket today. Yes, you will still owe whatever it is you owe, but at least the extra cash you pay in the form of excess income taxes withheld won’t be used to accelerate your debt payoff.

Some taxpayers have their refunds kept by the IRS because of back taxes, or other obligations such as student loans. In these situations, you can put yourself in a “tax due” position by decreasing your withholdings on your pay checks and putting more money in your pocket today. Yes, you will still owe whatever it is you owe, but at least the extra cash you pay in the form of excess income taxes withheld won’t be used to accelerate your debt payoff.

This is an oldie but a goodie. Speaking of liking cash: sell some of your profitable stocks along with your dogs. Not literally your dogs, but your under-performing securities. Sell enough to create a $3,000 gain and sell some more to add a $6,000 loss, and presto! You’ve pulled out some cash, yay, and created a $3,000 loss and tax deduction.

This is an oldie but a goodie. Speaking of liking cash: sell some of your profitable stocks along with your dogs. Not literally your dogs, but your under-performing securities. Sell enough to create a $3,000 gain and sell some more to add a $6,000 loss, and presto! You’ve pulled out some cash, yay, and created a $3,000 loss and tax deduction.

Here is another variant to the above year-end tax move: you sell securities whose price is stable yet is lower than what you paid. You use these losses to reduce the capital gains on securities you sold previously (profit harvesting). You wait 30 days to prevent wash sale triggers and re-purchase the securities that were sold at a loss (only if you believe it will eventually rebound in a timeframe that makes sense given inflation and other economic conditions).

Given market conditions now, this is a strong year-end strategy. There is another trick where you borrow against your unrealized gains. It is not necessarily a year-end tax move, however.

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

![[page_title]](https://wcginc.com/wp-content/uploads/Deduction-General.jpg)