Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

Table Of Contents

Real estate tax planning continues to evolve, and October’s focus is on practical plays that pair wealth building with tax efficiency. This month we stitched together four topics rental property owners and real estate investors ask about often: building a rental strategy that actually defeats PAL limits, the (sometimes spicy) conversion of STRs to personal use, why Qualified Improvement Property (QIP) matters for short-term rentals, and how to choose between bonus depreciation and Section 179 without stepping on a recapture landmine.

Keep in mind that all these blurbs are shrunk down versions of sections from our rental property book, “I Just Got A Rental, What Do I Do?”

Real estate investors often start with “what tax deductions can I take?” The foundation question is “how do I leverage those deductions?” If your modified adjusted gross income (MAGI) is above $150,000, you’re likely boxed in by passive activity loss (PAL) rules, and ordinary rental losses get suspended on Form 8582 unless you (a) qualify for REPS, (b) qualify for the STR loophole (≤7-day average stay with material participation), or (c) have other passive income to net against.

Once PAL limits are set aside with (a) or (b) above or you have a (c) situation, a cost segregation study can reclassify parts of the building to shorter-life Section 1245 property, enabling accelerated deductions. Layer in bonus depreciation (100% again for 2025–2030), and a $400,000 building might yield a $70,000–$90,000 first-year deduction in typical fact patterns. That’s cash-flow, not magic; you’re pulling future depreciation forward.

Sidebar: Where did the $70,000 to $90,000 come from? With 100% bonus depreciation, about 18% to 22% of the building will be accelerated. Where did the 18% to 22% come from? WCG CPAs & Advisors especially our Rental Expert Pod has seen thousands of cost segregation reports. We could say tens of thousands, but that would be a lie.

Supporting strategies—home office (to convert local trips from commuting to tax deductible business travel related to your rental property) and auto—can add smaller deductions. Just keep the Section 162 “ordinary and necessary” standard in mind; aggressive vehicle structures (e.g., luxury car self-rental from you to the rental) demand tight documentation and carry related-party risk. Finally, don’t forget maintenance days: when “substantially all” of a day is bona fide repair/maintenance, it generally doesn’t count as a personal-use day under vacation home rules—useful for lifestyle alignment without blowing the tax profile.

Speaking of blowing up, click on the button below to get the blown up version from our rental property book of this summary.

This is the edgy one: do a cost seg + bonus as an STR, then pivot to second home soon after. Can it work? Sometimes—but risk depends on timing and facts, and how another person (read, IRS agent) would view your intentions.

Key mechanics: Section 179 can be recaptured as ordinary income when business use falls to 50% or less (predominant use), potentially at the moment of conversion. Bonus depreciation typically avoids this midstream recapture (except for listed property like passenger autos and certain electronics, so basically unrelated to rental properties); instead, bonus is recaptured at sale unless you execute a 1031 like-kind exchange.

Risk spectrum:

Practical takeaway: if your long-term vision or retirement plan includes eventual personal use, bias to bonus depreciation over Section 179 and stretch the horizon to support legitimate business purpose and continuity.

Also mind state decoupling: many states disallow bonus depreciation but allow Section 179 (with limits). The optimal mix changes once you look at federal + state combined.

This one is often overlooked! Qualified Improvement Property (QIP) = interior, non-structural improvements to nonresidential buildings after the property is placed in service. QIP is 15-year property, so it’s eligible for bonus depreciation and also Section 179. The twist: a rental proeprty can be nonresidential when more than half of units are used on a transient basis—practically, an average stay of ≤30 days. That unlocks QIP treatment for things like kitchen and bath renovations (post-in-service date), which can be expensed via bonus (or Section 179 where appropriate).

Sidebar: Why does this rule mention “more than half the units?” There are common situations where commercial real estate has retail stores on the first floor with several floors above dedicated to residential (and in some cases, nonresidential) living. You could also have a large complex with many units, and some are short-term while others are mid- to long-term. For common real estate investors, this is a not an issue.

Caveats: touch structural framework, enlarge the building, or add elevators/escalators, and you’re out—those costs move to 27.5/39-year schedules depending on the residential versus nonresidential use. Sequence matters: (1) place the property in service as an STR (ready and available, advertised), (2) get actual guest stays to establish the STR profile, then (3) take it offline temporarily for qualified interior work. That ordering supports the nonresidential/QIP position.

Another Sidebar: Taking a rental property offline does not take the property out of service provided you intend to rent it again. This can be confusing. Once a rental property is placed in service for its intended income-producing purpose, it remains in service until the intent changes. This is a big deal when it comes to renovations since operating expenses can still be deducted during construction when the rental property is offline. Your material participation time continues as well!

Bonus vs Section 179 on QIP? Consider cash-flow needs, state conformity, entity-level traps (e.g., Section 179 can’t create a loss at the partnership level and is suspended at the entity, while bonus can create a loss), and whether future business use could dip below 50% (recapture risk for Section 179). And if you’re replacing HVAC / roof on nonresidential property: those aren’t QIP, but Section 179 may still apply via the statute’s carve-outs.

We just dropped a huge comment at the end with HVAC and roof replacements on nonresidential property under Section 179. There is a special carve out to allow for this. Click on the button below for a deeper dive.

This section from our book got a big makeover to include more examples, a fun table and some additional considerations. We hardly to it justice with this tiny recap-

Two primary tools compress time: bonus depreciation (IRC Section 168(k)) and IRC Section 179. After phasing down to 60% in 2024, bonus is scheduled at 100% for 2025–2030 under current law, the One Big Beautiful Bill Act. Bonus depreciation is unlimited, applies to property with ≤20-year lives, and can create losses (useful with REPS/STR). Section 179 is elective expensing with annual dollar limits, can’t create losses at the entity level (notably in partnerships), and is subject to recapture if predominant business use later falls to ≤50%.

Sidebar: Section 179 expenses that create losses on rental properties personally owned by you (or your revocable trust) and reported on Schedule E which also bypass passive activity loss limits with short-term rental loophole or real estate professional status can offset W-2 income. Read that again please since that is an incredibly long sentence but an important one. This same rental in a partnership (multi-member LLC, for example) is trapped.

Planning levers (sounds fancy):

Here is a great summary table from this section in our book-

| Asset (the thing you want to deduct) | 179 | Bonus | Notes |

| 5-Year and 7-Year Property | Yes | Yes | Standard 1245 property |

| Qualified Improvement Property (QIP, interior improvement) | Yes | Yes | Nonresidential only |

| Kitchen Reno, Bathroom Reno as QIP | Yes | Yes | Nonresidential only |

| Roof | Yes | No | Nonresidential, Sect 179 carve out |

| Furnace, Air Conditioner, Mini Split (HVAC) | Yes | No | Nonresidential, Sect 179 carve out |

| Appliances, Window Air Conditioner | Yes | Yes | Standard 1245 property |

| Water Heater (permanent) | No | No | Part of building, but have safe harbors |

| Water Heater (point of service, which is nice) | Yes | Yes | Standard 1245 property |

| Alarm, Security Systems | Yes | No | Nonresidential, Sect 179 carve out |

| Land Improvements (sidewalks, fences, landscaping, pools) | No | Yes | 15-year 1250 property |

| Temporary Fencing, Playground Equipment, Nets / Hoops | Yes | Yes | Standard 1245 property |

| Hot Tub (free-standing on slab) | Yes | Yes | Standard 1245 property |

| Hot Tub (in ground or integrated with deck) | No | Yes | Land Improvement, 15-year 1250 property |

| Foreign Rental Property | No | No | Not eligible outside U.S. |

Bottom line: you can mix Section 179 first, then apply bonus depreciation to the remainder for a tailored deduction profile—especially handy when coordinating entity limits, PAL outcomes, and state rules, and blah blah blah.

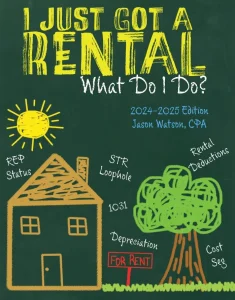

I just got a rental, what do I do? Purchasing a rental property is certainly challenging, but operating one to build wealth and find tax efficiency is equally challenging. This is our second book. Our first book, Taxpayer’s Comprehensive Guide to LLCs and S Corps, was first published in 2014 and was well-received by small business owners and tax professionals, so we thought a book on rental properties and real estate investments would be equally helpful. So, here we are with our second iteration, or the 2025 edition. We update it frequently throughout the year (last update was October 6, 2025).

I just got a rental, what do I do? Purchasing a rental property is certainly challenging, but operating one to build wealth and find tax efficiency is equally challenging. This is our second book. Our first book, Taxpayer’s Comprehensive Guide to LLCs and S Corps, was first published in 2014 and was well-received by small business owners and tax professionals, so we thought a book on rental properties and real estate investments would be equally helpful. So, here we are with our second iteration, or the 2025 edition. We update it frequently throughout the year (last update was October 6, 2025).

Our rental property book starts with entity structures and moves into asset management such as acquisition, cost segregation, rental safe harbors, repairs versus improvements, accelerated depreciation, partial asset disposition, and 1031 like-kind exchange. From there we discuss various rental considerations like passive activity losses, short-term rental loophole, real estate professional status, and material participation including what time counts, and what time doesn’t count.

Finally, the good stuff! Rental property tax deductions such as travel, meals, automobiles, interest tracing, home office and common expenses. Fun!

It is available in paperback for $19.95 from Amazon and as an eBook for Kindle for 15.95. Our book is also available for purchase as a PDF from ClickBank for $12.95.

If you buy our 480-page book and think that we didn’t help you understand rental property tax laws, let us know. We never want you to feel like you wasted your money. If you are ready to add some insightful reading into your day, click on one of the preferred formats. Amazon is processed by Amazon, and the PDF is safely processed by ClickBank who will email you the PDF as an attachment.

|  |  |

| $19.95 | $15.95 | $12.95 |

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.