Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

Posted Sunday, January 19, 2025

Table Of Contents

Many business owners are faced with the S corporation vs. C corporation business entity type selection conundrum. Interestingly, an S corporation is not an entity type but rather a tax election. To better understand the differences and to assist in the S corporation vs. C corporation question, let’s briefly run through a comparison table.

Many business owners are faced with the S corporation vs. C corporation business entity type selection conundrum. Interestingly, an S corporation is not an entity type but rather a tax election. To better understand the differences and to assist in the S corporation vs. C corporation question, let’s briefly run through a comparison table.

| LLC | Corporation | S Corporation | |

| Formation | Articles of Formation | Articles of Incorporation | NA |

| Internal Governance | Operating Agreement | Bylaws, Shareholder Agreement | Depends |

| Owners Called | Members | Shareholders | Depends (Shareholders) |

| Owners Own | Interest | Shares | Depends |

| Owners Take | Owner Draws | Owner Draws | Shareholder Distributions |

| Federal Tax Rate | 15.3% + Individual Tax Rate | 21% + Dividend Tax Rate | Payroll Tax + Individual Tax Rate |

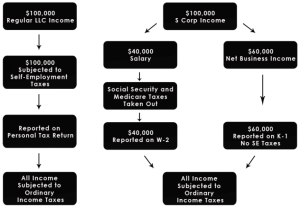

Why does an S Corp election exist? Well, we explained that earlier with a brief history lesson. More importantly, why does an S election exist in today’s climate? Easy! The near singular answer is the reduction of self-employment taxes. As mentioned everywhere on our website and our book, a garden-variety LLC that earns $100,000 after expenses could save $8,000 to $9,000 in taxes annually by leveraging the S corporation election. How?

As the graphic to the left explains, an S Corp election chops up the income between ordinary business income and reasonable shareholder salary. Your salary as a shareholder remains subjected to Social Security and Medicare taxes (which is the same as self-employment taxes). Your ordinary business income… what’s left after paying bills and your salary… is only subjected to income taxes and not self-employment taxes.

As the graphic to the left explains, an S Corp election chops up the income between ordinary business income and reasonable shareholder salary. Your salary as a shareholder remains subjected to Social Security and Medicare taxes (which is the same as self-employment taxes). Your ordinary business income… what’s left after paying bills and your salary… is only subjected to income taxes and not self-employment taxes.

In other words we parse away a chunk of business income and only subject it to income taxes while the rest is paid as a salary to the shareholders and is taxed with Social Security, Medicare and income taxes.

Naturally you want to keep your salary as low as possible to ultimately keep your overall S Corp taxes reduced. However, the IRS wants you to pay a reasonable salary which is a super squishy and grey number. And, you might want to bump up salaries to allow for larger 401k contributions and to also optimize your Section 199A deduction.

Click on the buttons below for more information on this… we don’t want to sidebar too deep within this article of S Corporations vs C corporations.

| S Corp Income | 100,000 | 200,000 | 300,000 |

| Salary | 40,000 | 80,000 | 120,000 |

| Payroll Tax | 6,120 | 12,240 | 18,360 |

| Income Tax | 6,980 | 24,150 | 44,266 |

| Total S Corp Taxes | 13,100 | 36,390 | 62,626 |

| C Corp Income | 100,000 | 200,000 | 300,000 |

| C Corp Tax | 21,000 | 42,000 | 63,000 |

| Dividends | 79,000 | 158,000 | 237,000 |

| Dividend Tax | 23,700 | 44,556 | |

| Total C Corp Taxes | 21,000 | 65,700 | 107,556 |

| Effective S Tax Rate | 13.1% | 18.2% | 20.9% |

| Effective C Tax Rate | 21.0% | 32.9% | 35.9% |

| Delta (extra tax because of C Corp) | 7.9% | 14.7% | 15.0% |

As you can see, a C Corp does not make sense after you add in capital gains tax on the dividends. This in turn makes sense — the lawmakers didn’t set out to kill S corporations. They set out to give every business owner a tax break. Gosh, half of Congress (535 doesn’t divide evenly, we get it) probably run S corporations on the side for their consulting and speaking gigs. C Corps remain a bad idea for tax efficiency.

Also note the effective tax rate (or labeled as tax “pain”) for the S corporation owner. At $100,000 in net business income, the total tax pain including payroll taxes is 13.1%, and at $200,000 it is only 18.2%. This is still well below the C corporation tax rate of 21%.

And! There’s more! C corporations do not enjoy the 20% Section 199A deduction either. Pile that onto the numbers above for even more reasons.

So, please pump the brakes on the “I wanna dump my S Corp for the magical tax arbitrage offered by a C Corp” nonsense. Wow, that was harsh. We did tell you to buckle up, but then we offended you by calling you buttercup. Safety with an insult.

As business entity types go, C corporations are not all bad. Here are some benefits:

One of the benefits is you keep income off your individual tax return (Form 1040). For example, if you had an LLC whose business transactions were typically reported on Schedule C of Form 1040, if you converted this LLC to a corporation, the income is contained in the corporate tax return (Form 1120). If you pay a salary or pay out dividends, that changes things. Why would you want to keep income off your individual tax return? Perhaps you have Social Security or disability benefits that might disappear or become taxable. Perhaps you are running away from some bad guys who are collecting on a debt. Maybe you use the C Corp to pay for your mistress of her expensive tastes. All kinds of reasons!

As mentioned elsewhere, the golden rule is: the person with the gold makes the rules. So, if you are looking for an investor to kickstart your heart like Nikki Sixx, and the only way it happens is if you create a C corporation, then that is what you do. All kidding aside, venture capitalists, angel investors, and all the other silly things people call themselves, like corporations as opposed to pass-thru entities (LLCs and S corporations).

As mentioned elsewhere, the golden rule is: the person with the gold makes the rules. So, if you are looking for an investor to kickstart your heart like Nikki Sixx, and the only way it happens is if you create a C corporation, then that is what you do. All kidding aside, venture capitalists, angel investors, and all the other silly things people call themselves, like corporations as opposed to pass-thru entities (LLCs and S corporations).

Having your employees own member interest in an LLC or S Corp can be tricky since each one would get a K-1 regardless if their interest was economic only (profits) or equity (ownership). You could get around this by having your employees own the right to a portion of the business which triggers into equity upon a certain event such as transfer of ownership or control. In other words, Employee A has the right to 2% ownership upon sale, partial or wholesale. This works! But, it can also be messy and hard to explain. WCG converted to a C corporation for this reason; we are selling bits and pieces of our business to partners and employees, and shares in a corporation makes more sense. Each partner is paid a fee for service directly from the corporation.

This is akin to a barrel of oil. You can either own the right to the barrel of oil, or the barrel of oil itself.

If you are a professional such as an attorney, accountant, medical doctor or engineer, you typically have to register as a professional entity, either a Professional LLC (PLLC) or a Professional Corporation (PC). However, some states, such as California, does not recognize PLLC and as such you must create a corporate that is deemed to be a PC. And in those cases, we typically recommend an immediate S corporation election to have your PC taxed as an S Corp (see crummy C Corp tax rates above).

Colorado and Texas, among several other states, allow for a PLLC or a PC, it’s up to you. WCG is a PC. We don’t want to digress too much here, since this article is about S corporations vs. C corporations. However, it’s important to understand that at times the conversation is moot since you must be a corporation, and the only remaining question is whether to elect S corporation status.

Who wants to pick on California some more? We do.

California allows corporate officers to opt-out of State Disability Insurance (SDI). SDI is California’s version of FMLA, and some business owners want to go on leave for new babies, etc. However, if your baby-making days are clearly in the rearview mirror, then perhaps you want to opt out of SDI. This is easily done, but only for corporate officers, and No, members of an LLC are not considered corporate officers since LLCs are companies not corporations. All in all, WCG creates far more corporations in California for this reason and for the PC designation reason.

If your estate plan attorney or another attorney recommends a corporation, ask the hard questions so you understand why. There might be good reasons to do so, and we leave room for attorneys to be right some of the time.

In summary, unless you fit the buckets above, then you should be an LLC or a C corporation taxed as an S corporation if business incomes warrant.

| Income | Total SE Tax | Salary | Total Payroll Tax | Delta | Delta% |

| 30,000 | 4,239 | 12,000 | 1,836 | 2,403 | 8.0% |

| 50,000 | 7,065 | 20,000 | 3,060 | 4,005 | 8.0% |

| 75,000 | 10,597 | 30,000 | 4,590 | 6,007 | 8.0% |

| 100,000 | 14,130 | 40,000 | 6,120 | 8,010 | 8.0% |

| 150,000 | 18,711 | 60,000 | 9,180 | 9,531 | 6.4% |

| 200,000 | 20,050 | 80,000 | 12,240 | 7,810 | 3.9% |

| 300,000 | 22,972 | 120,000 | 18,174 | 4,798 | 1.6% |

| 500,000 | 29,991 | 200,000 | 20,494 | 9,497 | 1.9% |

| 750,000 | 38,764 | 262,500 | 22,307 | 16,457 | 2.2% |

| 1,000,000 | 47,537 | 350,000 | 24,844 | 22,693 | 2.3% |

| 2,000,000 | 82,630 | 600,000 | 32,094 | 50,536 | 2.5% |

| 2,500,000 | 100,177 | 750,000 | 36,444 | 63,733 | 2.5% |

Don’t get too hung up on the drop in percentages. Focus on the overall hard dollar amount. Notice the sweet spot at $100,000 to $150,000 (yes, it dips at $300k due to Social Security limits). Also consider that if you run self-employed health insurance through the business (and you should), savings jumps up even more. Why? It has to do with the Social Security wage limit ($137,700 for the 2020 tax year) and we expand on this in our book titled Taxpayer’s Comprehensive Guide to LLCs and S Corps.

S Corp taxes are basically the payroll taxes paid on shareholder salaries plus the ordinary income taxes for each shareholder.

Bottom line savings is about 8-10% of your net business income after expenses for those earning $100,000. So, if you make $100,000 after expenses you’ll save about $8,000 to $10,000 in overall taxes, and they are all self-employment taxes. Self-employment taxes = Social Security / Medicare taxes = payroll taxes. All the same thing (in general). This is 8-10% number is just a jumping off point; as the table above shows, the percentage of savings goes down as income increases but the overall savings continues to rise, and can also increase to 12% to 15% depending on self-employed health insurance premiums and HSA contributions.

Bottom line savings is about 8-10% of your net business income after expenses for those earning $100,000. So, if you make $100,000 after expenses you’ll save about $8,000 to $10,000 in overall taxes, and they are all self-employment taxes. Self-employment taxes = Social Security / Medicare taxes = payroll taxes. All the same thing (in general). This is 8-10% number is just a jumping off point; as the table above shows, the percentage of savings goes down as income increases but the overall savings continues to rise, and can also increase to 12% to 15% depending on self-employed health insurance premiums and HSA contributions.

There is a cost to being an S corporation of course; all that glitters is only partially gold. Additional tax preparation fees for the corporate tax return and payroll processing are the two biggies. Still not convinced? No problem… please check out Line 4 from Schedule 2 on your Form 1040 tax return. This number reflects the self-employment taxes paid on your business income. We want to reduce this by 60 to 65% and we assume you do too!

Check out these S Corp resources as well:

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

![[page_title]](https://wcginc.com/wp-content/uploads/Reasonable-Salary.jpg)