Business Advisory Services

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us

Table Of Contents

There is a ton of chatter about time trackers and REPS logs including STR hours. Spreadsheets with dropdowns, conditional formatting, and built-in pivot tables. Neat. WCG CPAs & Advisors has a solution! But first, so much effort is spent on the right data that people lose sight of four fundamentals-

There is a ton of chatter about time trackers and REPS logs including STR hours. Spreadsheets with dropdowns, conditional formatting, and built-in pivot tables. Neat. WCG CPAs & Advisors has a solution! But first, so much effort is spent on the right data that people lose sight of four fundamentals-

Your time log must be done in real-time, or what the IRS considers contemporaneous. This is usually not a huge deal but it is surprising how many court cases mention that the records were not kept in real-time.

Next, your time log must highlight not just your time, what you did and the location, it must also contain the time spent by others on your rental activities. This demonstrates your exhaustiveness or completeness in recording all time spent, not just yours.

Next, your time log must appear credible. To support credibility, you will likely need to recall details surrounding the time or moments spent. You will also need to be reasonable. In Escalante v. Commissioner, Tax Court Summary Opinion 2015-47, the rental property owner listed hundreds of hours for writing checks and reviewing mortgage statements. The Tax Court considered how long it would take them to write their own checks based on their own experience of daily life.

Finally, your time log must be corroborated with other transactions or by disinterested third parties. You claim that you spent 6 hours replacing a toilet, and you also demonstrate two separate trips to Lowe’s with receipts. The first is the toilet. The second has all the crud that you forget to get the first time. Perfect! However, in Pourmirzaie v. Commissioner, Tax Court Memo 2018-26, the rental property owner’s time log showed her being at the rentals every single Saturday performing “weekly cleaning and repairing” work. Unfortunately, her bank and credit card statements showed purchases in other locations besides her rental properties. Oops.

There are several time tracker apps, Excel templates and the like. We routinely get asked two questions- who is your cost seg referral, and how should we track our time for real estate professional status or short-term rental loophole? The first one is easy- we continue to recommend Andy and his team at CostSegEZ.com.

There are several time tracker apps, Excel templates and the like. We routinely get asked two questions- who is your cost seg referral, and how should we track our time for real estate professional status or short-term rental loophole? The first one is easy- we continue to recommend Andy and his team at CostSegEZ.com.

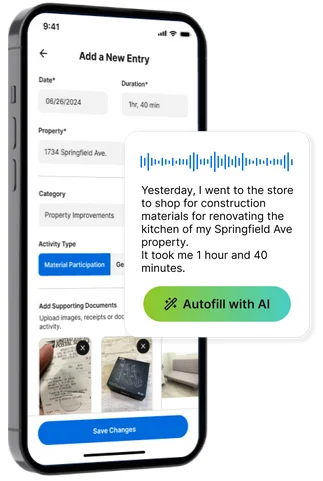

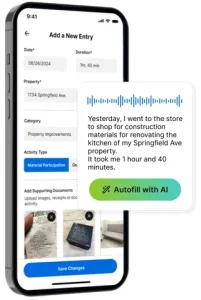

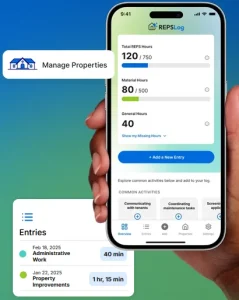

For time tracking, whether REPS or STR, we have partnered with REPSLog.

Don’t let the title fool you- while tracking time for REPS is a bit more exhaustive given the 750 hours in real estate activities requirement in addition to material participation in the rental activities, it can easily track time for STR loophole needs (average guest stay of 7 days or less + material participation). As a refresher, there are 3 primary ways to achieve material

In speaking to the founders of REPSLog recently, they are rolling out STR capabilities within their app as well.

In speaking to the founders of REPSLog recently, they are rolling out STR capabilities within their app as well.

As mentioned above in fundamental #4, your STR or REPS log must be corroborated. This is akin to a mileage log. It is a common misconception that just a mileage log is all you need to defend your automobile expenses. Not true. You also need corroboration such as service receipts from your dealership or Jiffy Lube supporting beginning and ending odometer reads.

Is a time log always required? No. Treasury Regulations Section 1.469-5T(f)(4) reads-

Is this suggesting that a written log is not needed if participation can be established by other means? Yes. But be careful!

Here is a win for the real estate investor. In Birdsong v. Commissioner, Tax Court Memo 2018-148, the taxpayers did not maintain contemporaneous records but testified credibly to their activities. Here is a blurb from the ruling-

Petitioners testified credibly and in detail about petitioner wife’s active and extensive management of their rental properties. Furthermore, petitioners presented detailed spreadsheets that reflected petitioner wife’s rental management activities exceeded the 750-hour requirement. We find petitioners’ narrative summary and thorough time logs convincing because petitioners owned numerous rental units that petitioner wife operated alone. See Hailstock v. Commissioner, (holding that the taxpayer’s credible testimony regarding time spent operating multiple properties alone satisfied the section 469(c)(2) requirements). Petitioners’ testimony is further buttressed by petitioner wife’s thorough time-keeping as well as the receipts and invoices petitioner wife produced to corroborate her time logs.

Petitioners testified credibly and in detail about petitioner wife’s active and extensive management of their rental properties. Furthermore, petitioners presented detailed spreadsheets that reflected petitioner wife’s rental management activities exceeded the 750-hour requirement. We find petitioners’ narrative summary and thorough time logs convincing because petitioners owned numerous rental units that petitioner wife operated alone. See Hailstock v. Commissioner, (holding that the taxpayer’s credible testimony regarding time spent operating multiple properties alone satisfied the section 469(c)(2) requirements). Petitioners’ testimony is further buttressed by petitioner wife’s thorough time-keeping as well as the receipts and invoices petitioner wife produced to corroborate her time logs.

On the basis of petitioners’ testimony and the record as a whole, we conclude that petitioner wife, pursuant to section 469(c), materially participated and is a real estate professional. Accordingly, petitioners’ loss attributable to their rental real estate is not limited by the passive activity loss rules of section 469.

But the Tax Court also gave a little spanking in a footnote-

Although we caution petitioner wife to construct more strictly contemporaneous time logs for her future endeavors, we find her credible testimony and time logs to be a “reasonable means” of proof. See sec. 1.469-5T(f)(4), Temporary Income Tax Regs., 53 Fed. Reg. 5727 (Feb. 25, 1988).

Take the win! At the risk of de-emphasizing time logs, recall that in Hailstock v. Commissioner, Tax Court Memo 2016-146, the rental property owner did not keep a time log with specific hours. The Tax Court accepted her narrative and stated “we find petitioner’s narrative summary convincing because she owned numerous rental properties and conducted her business as a “one-man operation” without being otherwise employed.”

Keep a time log please! Use a time tracker like REPSLog.

Table Of Contents

Tax planning season is here! Let's schedule a time to review tax reduction strategies and generate a mock tax return.

Tired of maintaining your own books? Seems like a chore to offload?

Everything you need to help you launch your new business entity from business entity selection to multiple-entity business structures.

Designed for rental property owners where WCG CPAs & Advisors supports you as your real estate CPA.

Everything you need from tax return preparation for your small business to your rental to your corporation is here.

WCG’s primary objective is to help you to feel comfortable about engaging with us